Being in relationship with linear equations

In this section we will be covering following things:

1. Regression in linear equations

a. Simple Linear Regression

b. Multiple Linear Regression

2. Correlation coefficient

a. Equation of correlation coefficient

b. Example problem on correlation coefficient

3. Residuals

a. Intuition behind residual

b. Example problem on residual

4. Coefficient of determination

1. Regression in linear equations

IRegression is a statistical method used in finance, investing, and other disciplines that attempts to

determine the relationship between one dependent variable (usually denoted by Y) and a series of other

variables (known as independent variables).

The two basic types of regression are simple linear regression and multiple linear regression, although

there are non-linear regression methods for more complicated data and analysis.

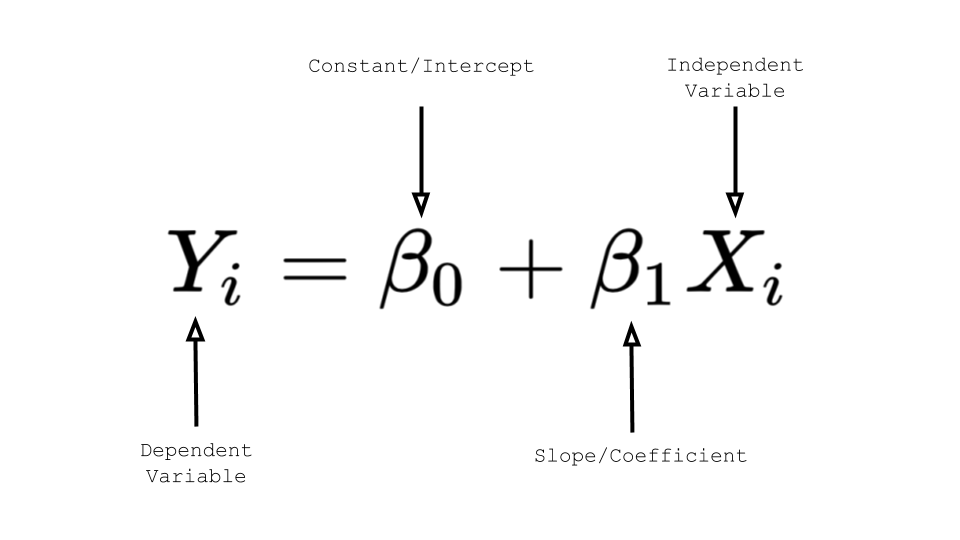

a. Simple linear regression

Simple linear regression has only one x and one y variable i.e one dependent variable and

one independent variable. For instance, when we predict rent based on square feet alone

that is simple linear regression.

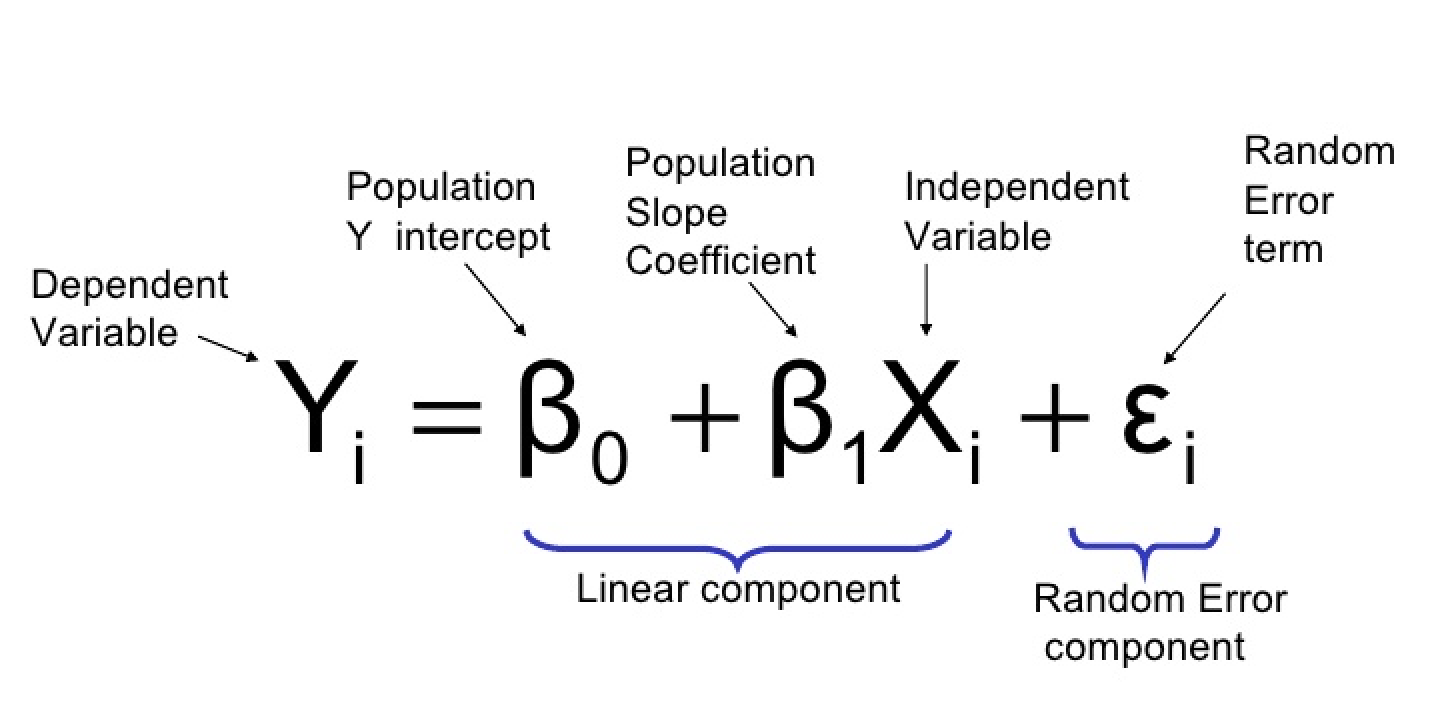

b. Multiple Linear regression

Multiple linear regression has one y and two or more x variables i.e one independent

variable and two or more dependent variables. For instance, When we predict rent based on

square feet and age of the building that is an example of multiple linear regression.

2. Correlation coefficient

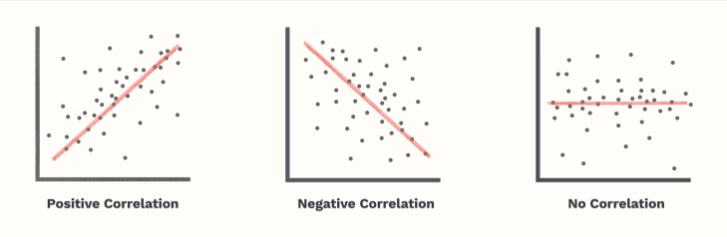

* The correlation coefficient is a number calculated from given data that measures the strength and

direction of the linear relationship between two variables: x and y.

* The sign of the linear correlation coefficient indicates the direction of the linear relationship

between x and y.

* When r (the correlation coefficient) is near 1 or −1, the linear relationship is strong; when it

is near 0, the

linear relationship is weak.

A univariate normal distribution is described using just the two variables namely mean and variance. For a

multivariate distribution we need a third variable, i.e., the correlation between each pair

of random variables.

a. Equation of correlation coefficient

The strength of the linear association between two variables is quantified by the correlation coefficient.

Given a set of observations (X1, Y1), (X2,Y2),...(Xn,Yn), the formula for computing the correlation

coefficient is given by

where Sx and Sy stands for standard deviation for variable x and y respectively.

From the above formula we can see that it somehow looks like a z score. We can write

the same equation as follows:

b. Example problem on correlation coefficient

Problem: Given following data points which consist of 2 variables x and y find the correlation coeff.

(X,Y)

( 1, 1)

( 2, 2)

( 2, 3)

( 3, 6)

Solution:

The dataset has 2 dimension or 2 variables, Those are x and y

x = [ 1, 2, 2, 3]

Mean can be calculated as: X̅ = ( 1+2+2+3 ) / 4 = 2

Standard deviation: Sx = 0.816

y = [ 1, 2, 3, 6]

Mean can be calculated as Ȳ = ( 1+2+3+6 ) / 4 = 3

Standard deviation: Sy = 2.16

Hence r = [ ( X 1 - X̅ ) / Sx * ( Y 1 - Ȳ ) / Sy

+ ( X 2 - X̅ ) / Sx * ( Y 2 - Ȳ ) / Sy

+ ( X 3 - X̅ ) / Sx * ( Y 3 - Ȳ ) / Sy

+ ( X 4 - X̅ ) / Sx * ( Y 4 - Ȳ ) / Sy] / n-1

Hence r = [ ( 1 - 2 ) / 0.816 * ( 1 - 3 ) / 2.16

+ ( 2 - 2 ) / 0.816 * ( 2 - 3 ) / 2.16

+ ( 2 - 2 ) / 0.816 * ( 3 - 3 ) / 2.16

+ ( 3 - 2 ) / 0.816 * ( 6 - 3 ) / 2.16] / 4-1

r = 0.946

3. Residuals

a. Intuition: Residual is difference between actual and predicted.

residual = Σ (actual - predicted )

sum of residual squares = Σ (actual - predicted )^2

When we are trying to find the line that best fits our data set we are trying to reduce the residuals

or we can also use sum of residuals for the minimisation task.

b. Example problem on redidual

Problem: Vera rents bicycles to tourists. She records the height (in cm) of each customer

and the frame size (in cm) of the bicycle that customer rented.

After plotting her results, Vera noticed that the relationship between the 2 variables was fairly linear,

so she used the data to calculate the following least square regression equation for predicting the

bicycle frame size from the height of the customer:

y = 0.33 + 0.33 x

What is the residual of a customer with a height of 155 cm who rents a bike with 51 cm frame ?

Solution:

actual frame size = 51 cm

predicted frame size:

y = 0.33 + 0.33 x

= 0.33 + 0.33*155

predicted = 51.48 cm

residual = actual - predicted

= 51 - 51.48

= -0.48 cm

Hence the residual is -0.48 cm

4. Coefficient of determination

The coefficient of determination is a measurement used to explain how much variability of one factor can

be caused by its relationship to another related factor. This correlation, known as the "goodness of fit,"

is represented as a value between 0.0 and 1.0.

In statistics, the coefficient of determination, denoted R² or r² and pronounced "R squared", is the

proportion of the variation in the dependent variable that is predictable from the independent variable.

Given X and Y where Y is dependent variable and X is dependent variable. Ȳ represents the mean of Y

and X̅ represents the mean of X

- Total variation in Y can be defined as Squared Error from Average Ȳ

SEy = ( Y1 - Ȳ )² + ( Y2 - Ȳ )² + ..................... + ( Yn - Ȳ )²

- Variation that is NOT predictable from independent variable can be defined as:

SELINE = ( Y1-(mX1 +b) )² + ( Y2-(mX2 +b) )² + ............. + ( Yn -(mXn +b) ) ²

- Proportion of Variation that is NOT predictable from independent variable can be defined as:

SELINE/SEy

- Proportion of variance that is predictable from independent variable ( r² ) is

= 1 - Proportion of Variation that is NOT predictable from independent variable

= 1 - (SELINE/SEy )

r² = 1 - (SELINE/SEy )

Correlations are good for identifying patterns in data, but almost meaningless for quantifying a model’s

performance, especially for complex models (like machine learning models). This is because correlations

only tell if two things follow each other (e.g., parking lot occupancy and Walmart’s stock), but don’t tell

how they match each other (e.g., predicted and actual stock price).